Artificial intelligence has handed fraudsters deepfakes, cloned voices, and near-perfect forged deeds. Here's how AI deed fraud works in Florida, who's most at risk, and the concrete steps — owner's title insurance and free county fraud alerts — that protect your property.

Margaret Jimenez, owner of Aventura title agency All Star Title, was arrested in Pembroke Pines and accused of stealing over $300,000 in escrow from a client. We explain what's alleged, why escrow can be a target, and how a Closing Protection Letter protects your closing money.

FHFA Director Bill Pulte says Fannie Mae will expand its title waiver pilot. What the program covers, why it's limited to certain refinances, and what it means for your closing.

A First American white paper estimates up to $1 trillion in annual title risk if title insurance is weakened — and explains why the work happens before a claim is ever filed.

A title company's plain-English recap of the laws and funding from Florida's 2026 sessions — anti-fraud protections, the new property tax estimator disclosure, homebuyer assistance dollars, and what each means for your closing.

Behind every closing sits an invisible system of property records — and title insurance is a large part of what keeps it accurate. Why that matters far beyond your own transaction, and what it means for Florida buyers.

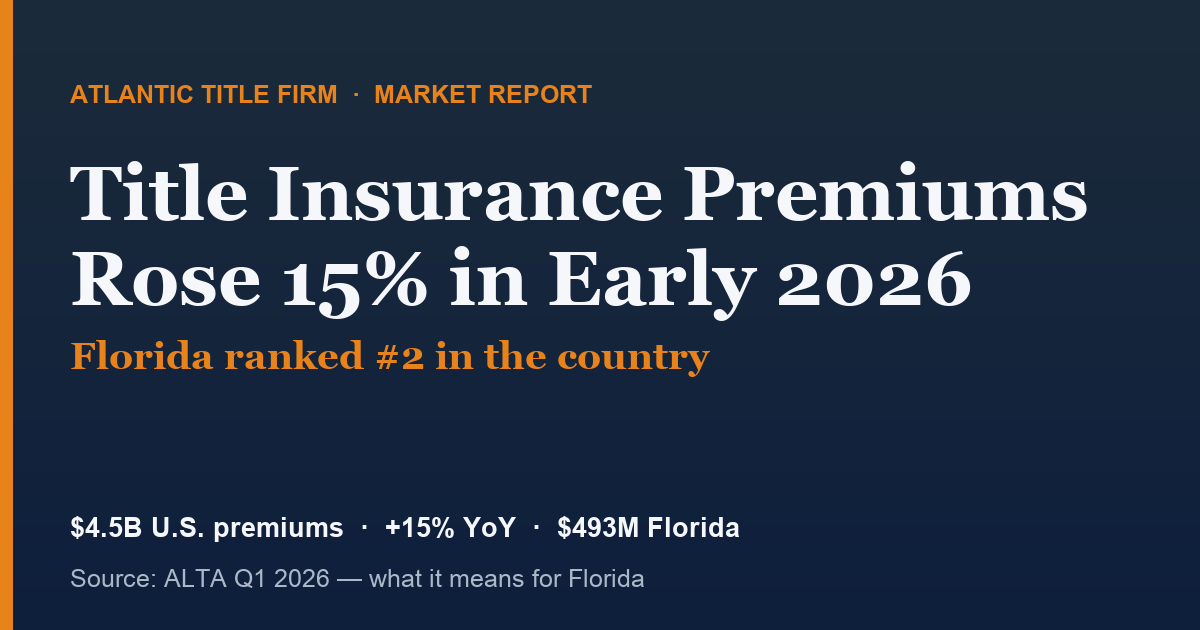

ALTA reports U.S. title premiums jumped to $4.5B in Q1 2026 while claims fell — and Florida ranked #2 nationally with ~$493M. What rising premiums (but fixed Florida rates) mean for buyers and sellers.

A Palm Beach law firm's lawsuit alleges millions vanished from its escrow account through unauthorized wires. We break down how real estate wire fraud works, how to protect your closing funds, and what to do in the first hours if you're targeted.

Florida fixes title insurance rates — but the Butler rebate lets a title agent legally refund part of their commission to you at closing. How it works and how much you can save.

Westcor promoted Lina Athanasiou to Florida commercial underwriting manager — plus a plain-English guide to what commercial title underwriting means for your deal.

Over 1,100 builders pressed Congress on affordability and supply. A plain-English breakdown of the four priorities — and what they could mean for Florida buyers, sellers, and closings.

A Texas court struck down FinCEN's residential real estate reporting rule — then FinCEN appealed. What the legal back-and-forth means for Florida title companies and all-cash entity buyers.

The bank's policy only protects the bank, Florida title rates are set by the state, and three more myths that cost homebuyers thousands — with a 45-second explainer video.

A 2026 snapshot of Florida home values and the fastest-growing counties — plus the brokerages and agents moving the most real estate statewide (RealTrends data).

From mega firms like The Real Brokerage, LPT Realty, and the Keyes Company to the best boutique companies in every metro — a statewide directory with a link to each.

Pending association litigation, liens, a lis pendens, structural-defect suits, and quiet title disputes can all stall a condo closing — the 5 things to watch for, and how to stay protected.

Wire fraud, last-minute credit changes, insurance timing, who pays what, and the homestead signing trap — the errors that delay or kill Florida closings.

Title fees, the HOA estoppel fee, the property-tax reassessment trap, recording fees, and escrow prepaids — the closing costs buyers don't see coming.

Open permits, garage conversions, and DIY additions can stall your closing and create liens. How to spot the risk and protect your purchase.

Do you need probate to sell an inherited Florida home? How Lady Bird deeds, trusts, and clear title affect the sale — in plain English.

The honest version of deed fraud — how it works, why free county property fraud alerts and an owner's title policy protect you, and whether you need a paid title lock.

What to bring, what to confirm before you sign, and how to avoid wire fraud — a printable closing-day checklist for Florida buyers.

What "independent" really means, your right to choose your own title company, and why Florida title rates are the same everywhere — 5 things every buyer and seller should know.

The neutral professional behind every clean Florida closing — what they do, how it differs from a real estate agent, and why it matters.

A step-by-step Florida guide — eligibility, the pre-licensing course, the state exam, fingerprinting, appointment, and how to land your first title agent job.

The pre-licensing course, state exam, fingerprinting, appointment, and continuing education that go into getting and keeping a Florida title agent license.

Buying or selling Florida property from out of state? Here's how a mail-away closing works — you sign locally, we handle the rest — plus how it compares to RON.

Selling by owner? This step-by-step checklist takes you from accepted offer to recorded deed — title, disclosures, deed prep, HOA estoppel, and closing day.

Title insurance is one of the most important protections a Florida homebuyer can have — yet many buyers don't fully understand what it covers or why it matters. Here's what you need to know before closing.

Buying or selling in Florida? Understanding the closing process helps you avoid surprises and ensures a smooth transaction from contract to keys.

Florida is a leader in RON closings. If you can't attend your closing in person — or just prefer the convenience — here's how remote digital closings work.

Real estate investors in Florida face unique title challenges. From assignment of contracts to simultaneous closings, here's how to protect your deals.

FSBO sellers in Florida still need a title company. Atlantic Title Firm explains the title and closing requirements for selling your home independently.

Our title agents across Florida share what they're seeing on the ground — from Florida's hot condo market to booming Central Florida suburbs.

A plain-English guide to how title insurance works, what it protects, when you buy it, and how long the coverage lasts.

The full 2026 promulgated rate chart — owner's policy premiums from $200K to $1.5M, the same statewide-regulated rates we use on real closings.

Real Florida title-defect scenarios, why a lender's policy alone leaves the buyer exposed, and the rare cases where skipping it makes sense.

What each policy covers, who's protected, who pays, and the simultaneous-issue discount — a full Florida comparison.

Every covered scenario — forgery, fraud, missed liens, undisclosed heirs, encroachments, recording errors — plus what it does not.

How they differ: one-time vs annual premium, past events vs future events. A quick guide so Florida buyers don't confuse the two.

Selling by owner? Here's how title search, escrow, deed prep, and settlement work — and why you still need a title company.

In Florida, whoever pays for owner's title insurance picks the closing agent — and county custom decides who pays. Here's how to negotiate it.

Do FSBO sellers need title insurance, and what does it cost? Promulgated rates, who pays by county, and sample calculations.

A line-by-line breakdown: doc stamps, title insurance, recording, settlement fee, and HOA estoppel — with a free calculator.

What Florida law and your contract actually say about funds, possession, and the key handoff at the closing table.

Why Florida searches title all the way back to the 'root,' what we examine, and how it protects your purchase.

How to read Schedule A and Schedule B — what the commitment actually means for buyers, sellers, agents, and lenders.